A Very Special Dividend

“The solution to pollution is dilution.” – Anonymous

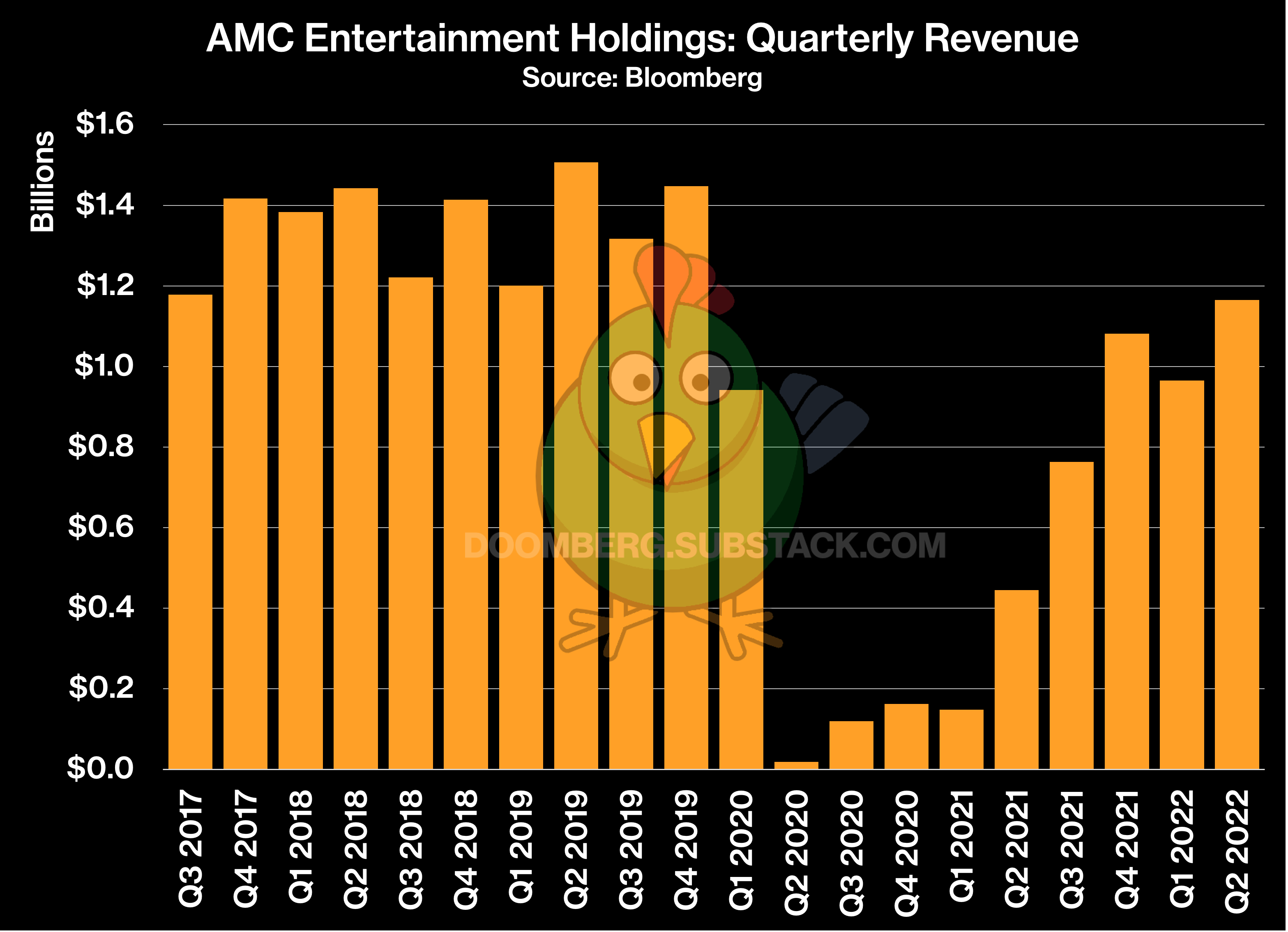

By most measures, the second quarter of 2022 was a banner season for movie theater operators. Top Gun: Maverick was a record-breaking success among a cavalcade of high-profile blockbusters. More importantly, Tom Cruise’s classic reprise reminded people that going to the theater and seeing action on the big screen – feeling it, really – can be absolutely awesome. For AMC Entertainment Holdings (AMC), North American box office numbers were the strongest they have been since 2018. On the company’s earnings call last Thursday, CEO Adam Aron was more than happy to spike the football (transcript via Bloomberg, emphasis added throughout):

“I have said all along that people would come back to theaters in the eye-popping numbers, and that is exactly what they did in the second quarter 2022 and what they've been doing since. To the naysayers who, flawlessly in our opinion, have been predicting a secular decline of theatrical exhibition, all I can say is, well, you've seen my feisty hashtags on Twitter. You know what I say.”

While we can’t say for sure which feisty hashtags Aron was referring to, we suspect he had these two favorites in mind during the call with analysts – #LetThemEatCrow and #CHOKEonTHAT. Such is the nature of polite discourse from prominent business leaders in 2022.

Inspecting a chart of AMC’s revenue does indeed suggest the company is on track to reach pre-pandemic levels, although compared to the same quarter in 2019, sales were still down 22%.

Despite the tailwinds at the top-line, AMC lost money and continues to hemorrhage cash. The company’s earnings press release proudly proclaimed, “Operating Cash (Burn) Generated for the quarter was a positive $52.0 million,” with a footnote that helpfully defines this term as, “Operating Cash (Burn) Generated is a non-GAAP metric that represents cash burned or generated before debt servicing costs and before deferred rent payback.” When management serves up wildly massaged non-GAAP measurements like these, we prefer to keep things simple: GAAP net loss was $122 million and the company’s cash balance dropped by $200 million.

To survive the pandemic and avoid what we believe was a necessary and still inevitable bankruptcy filing, Aron diluted existing shareholders so forcefully it bordered on the obscene. By more than quintupling the number of common shares outstanding, AMC raised $3.2 billion in cash from financing over the past 10 quarters, but only $965 million remains on the balance sheet ($746 million if you net out the deferred rent remaining to be paid). The impact of this dilution can be best visualized by plotting the revenue on a per share basis. While the company’s revenue may have largely recovered to pre-Covid levels, the per share claim on that revenue is barely 15% of what it was in the same quarter of 2019:

Aron’s antics and promotional behavior aside, AMC is a loss-making enterprise with $5 billion in debt. Its 10% coupon bond due in October of 2026 currently fetches a 16% yield in the open market, implying the debt markets are now closed to the company. Having blown through more than $600 million in the first six months of 2022 alone, Aron needs to raise more cash from the equity markets – and soon. But therein lies the rub. The same retail crowd the company has cynically leveraged to stay afloat has loudly rejected Aron’s desire to further dilute his shareholders. Last year, he was forced to table a motion seeking approval to sell more stock at AMC’s 2021 annual meeting. At the 2022 meeting held less than two months ago, he ruled out tapping the markets for the remainder of the year:

“AMC Entertainment hosted its annual stockholders meeting on June 16. The agenda included shareholder votes on three key proposals as well as the discussion of other matters relevant to AMC's ongoing business strategy.

During that latter section, AMC announced that it has no plans to issue new equity in 2022. That proclamation drew positive attention from AMC retail investors.”

Such are the circumstances that led to Aron’s latest gambit. In releasing the company’s second-quarter results last Thursday, AMC also announced it would issue a special dividend of preferred equity units to each of the company’s shareholders. Surfacing a shareholder-approved authorization ratified back in 2013, the move caused some confusion among its predominately retail shareholder base. However, 2022 being what it is, the stock finished up 19% on Friday. When in doubt, buy stonks. What is the nature of this “special dividend” and what is Aron’s real motivation for the move? Let’s dig in.