Flashing Orange

A cheat sheet for a potential European natural gas crisis.

“Because, of course, the least expensive energy is the energy that is not used.” – Ursula von der Leyen

At its zenith, the German nuclear power sector was the envy of the world. By the turn of the century, the country operated 19 of the most sophisticated and reliable nuclear reactors on the planet, churning out 170 terawatt-hours (TWh) of baseload electricity per year. With proper care and maintenance, these facilities could have been effectively immortal, a perpetual anchor to a globally elite economy. What followed—which is well-trodden territory in these pages—was one of the greatest own goals in geopolitical history.

Those 170 TWh of power would come in handy for the European Union (EU) now, as it stares down the barrel of what looks increasingly likely to become the greatest energy crisis of this generation. While much attention will understandably be paid to upcoming regional stockouts of jet fuel and diesel—and the degradations to modern life they will trigger—a slower-rolling yet equally challenging crisis is unfolding. In a scandal that defies belief, the member states of the EU have exited the winter of 2025–2026 with disastrously low stores of natural gas just as the war in Iran has closed the Strait of Hormuz, taking 20% of the world’s supply of liquefied natural gas (LNG) offline.

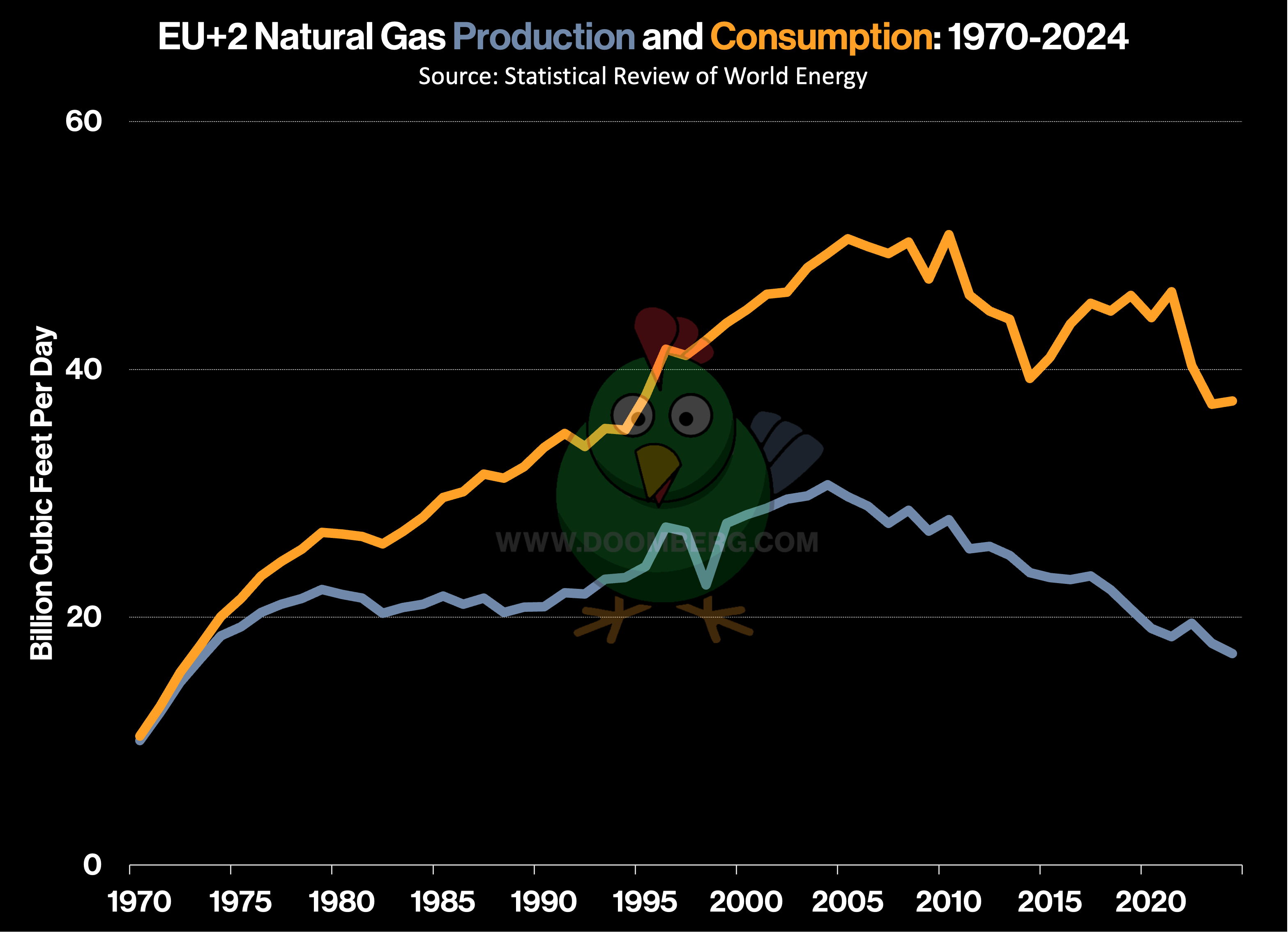

To quantify the scale of the challenge, it is best to combine the production and consumption statistics of the EU, Great Britain, and Norway (collectively, the EU+2). The latter two, the largest natural gas producers in Europe, are not members of the EU itself but are fully connected to it via pipeline. A quick perusal of the Statistical Review of World Energy indicates that the EU+2 produces less than half the gas it consumes, a gap of roughly 20 billion cubic feet per day (bcf/d). This is approximately equivalent to the entire natural gas output of the mighty Permian Basin.

As the refilling season begins in earnest, there is little room for error and no tolerance for a long, drawn-out war in the Middle East. A bad outcome is all but guaranteed—energy prices will rise, and deindustrialization will continue—but whether a true catastrophe can be avoided is the question at hand.

Gauging the EU’s progress on its upcoming journey requires mapping major gas inflows, assessing whether those pathways are in significant jeopardy, and listing the risks to keep a close eye on as geopolitical developments evolve. Having done this work over the past week, we present our findings here.