Liquefied Natural Glut

On the inelasticity and interdependence of primary energy markets.

“I've seen gluts not followed by shortages, but I've never seen a shortage not followed by a glut.” – Nassim Taleb

What do precipitation levels in Sichuan have to do with the price of coal in Appalachia? As odd to ponder as it is simple to formulate, answering this question lays bare two realities: as a whole, the demand for primary energy is highly inelastic, and the sources available to meet that demand have a meaningful degree of fungibility. Coal, natural gas, oil, uranium, dammed water, biomass, wind, and solar can each be used to produce electricity, for example, and all that matters is that the lights come on with good reliability. Taken together, these forces mean small shortages of energy can lead to huge price increases (and vice versa), and such price action is often swiftly transmitted across global fuel markets.

Back to the rain in Sichuan: We were motivated to elaborate on its connection to energy prices after reading an article published in early November by the Syncretica Substack. Straightforwardly titled “Chinese Hydropower – Large and Underappreciated,” the author observes that increased rainfall in southern China was putting downward pressure on global coal prices. Here are a few key excerpts (emphasis added throughout):

“Hydropower is a major driver of Chinese imports of coal and gas due to China’s grid topology. The provinces in China that are part of the Southern Grid do not have substantial coal resources of their own and their imports swing wildly based upon hydro power performance…

Rainfall has picked up materially recently and China’s hydropower output based upon current and forecast weather is likely to improve a great deal…

The implication here is that China has built a large stockpile of coal recently just as the weather turned implying much weaker fossil import demand until the weather changes again or those inventories are worked off.”

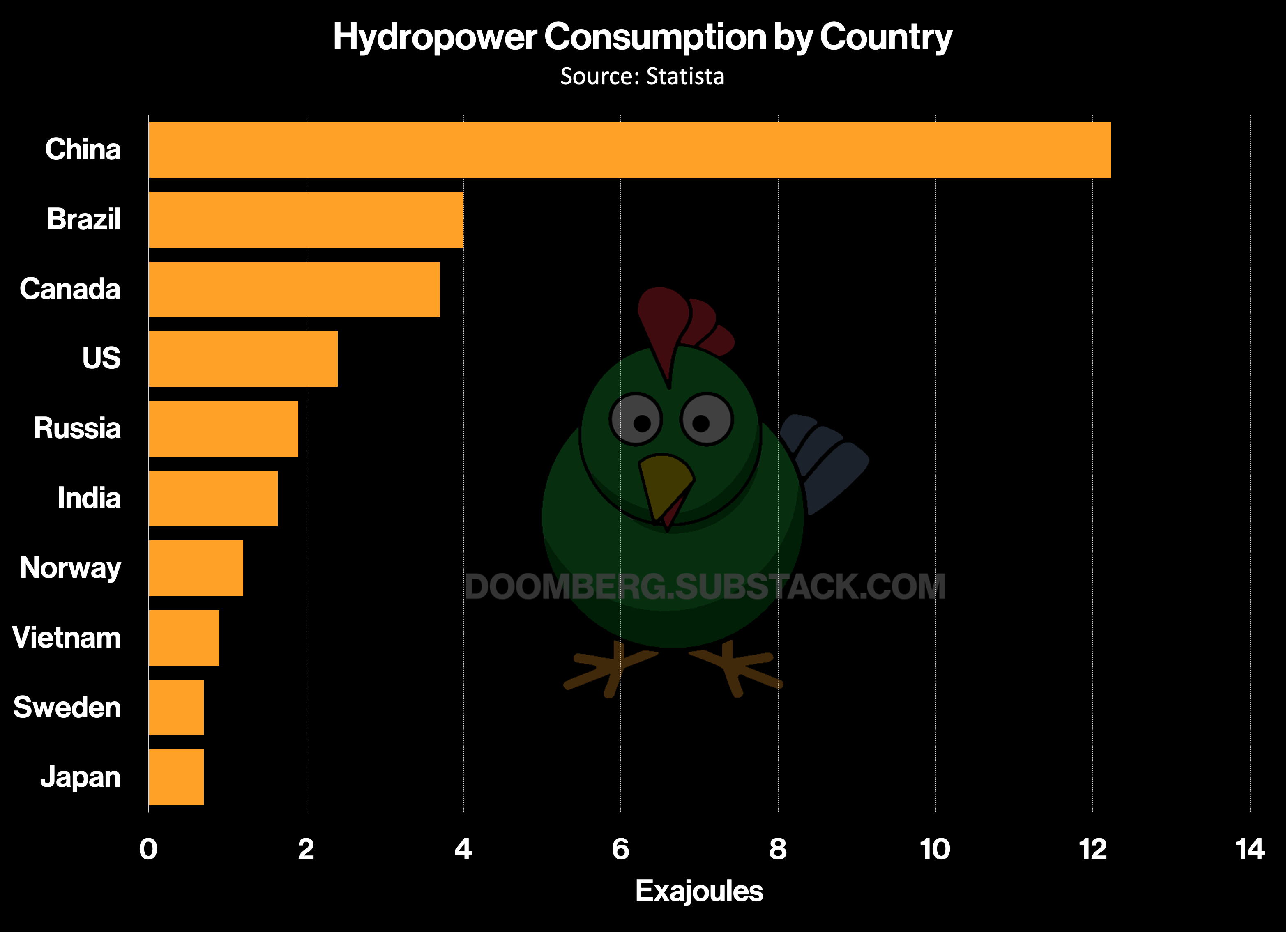

China’s hydropower footprint is indeed quite large, accounting for slightly more than 2% of all primary energy consumed worldwide. Its share is equivalent to the entire energy consumption of Germany and is greater than the total utilized by all but 10 countries. With prices set at the margin, swings in the weather in China nudge (and sometimes push) the price of coal in Asia, and since coal is a globally traded commodity with ruthlessly efficient logistics, perturbations in Chinese hydropower production thus permeate across the entire primary energy complex.

The global energy crisis of 2021-2022, which began when Europe flubbed its natural gas storage strategy in the spring of 2021, led to substantial tailwinds for the price of all fossil fuels. Following the outbreak of war in Ukraine in February of 2022, the situation went from bad to desperate, with natural gas, coal, and oil prices all soaring to nosebleed heights, essentially in lockstep. As we have previously estimated, Europe had been receiving roughly 15 billion cubic feet per day (bcf/d) of natural gas from Russia, and much of that supply was eventually cut off. This interruption forced Europe to find new supply in a global market that consumed approximately 377 bcf/d, of which 50 bcf/d was accessible in the liquefied natural gas (LNG) market. Europe’s deficit set off a worldwide scramble for energy of all forms, and it was only through Herculean efforts and the blessing of an unusually warm winter that the worst for the continent was avoided. The damage done to global economies reverberates to this day.

Extreme energy shortages—and the price trends that follow—inevitably trigger a wave of over-investment by commodity producers caught up in the frenzy. The temptation to draw tangent lines to sine waves seems universally irresistible, and a tsunami of new natural gas projects is coming online just as the global energy dynamic is stabilizing. In the November edition of our Pro tier Doom Zoom presentation—“Simple Molecule, Complex Markets: A Comprehensive Review of Natural Gas”—we performed a deep dive into this vital molecule. What we found will give energy bulls pause. Let’s peruse some of the highlights.