Nickel In Front of a Steamroller

“A nickel ain't worth a dime anymore.” – Yogi Berra

On Monday, March 22, 2021, ViacomCBS (since renamed Paramount Global) announced plans to raise money from the equity markets. For reasons few could understand, the company’s stock had soared from a Covid-panic low of about $10 a share a year earlier to around $100 at the time of the stock offering. Taking this as a signal of confidence from the market, management made the rational decision to raise money to accelerate and de-risk its execution plans. The company hired Morgan Stanley to be the lead book runner on the deal and hoped to secure $3 billion in fresh capital.

Raising capital for companies is a core function of banks, and casual observers might assume such activities represent the bulk of what bankers do. They’d be wrong. As the scandal following the subsequent collapse in ViacomCBS’s stock laid bare, bankers expend a lot of effort on – and collect a lot of fees from – facilitating games of reckless speculation, often skirting the law to do so.

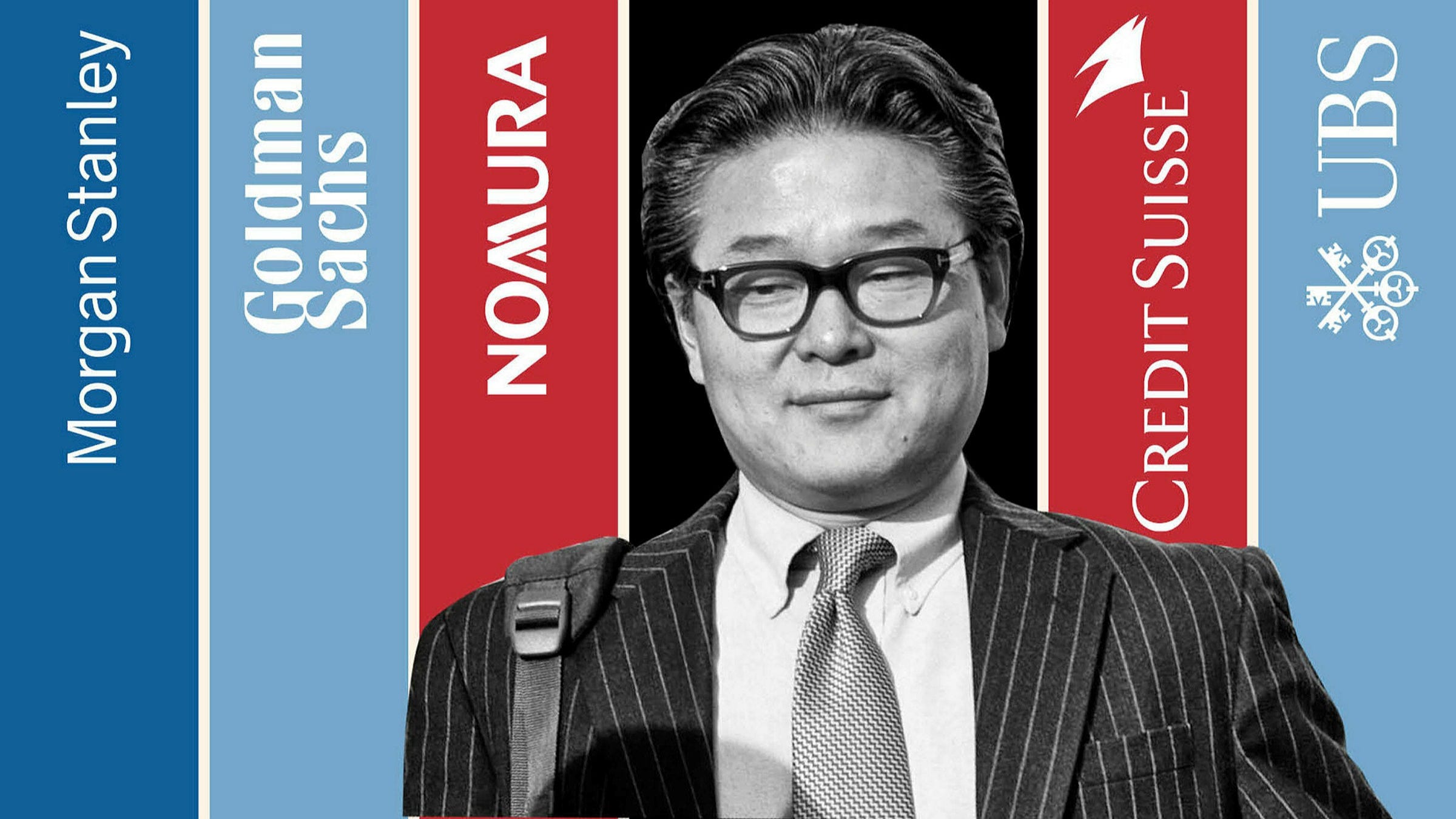

Unbeknownst to the management of ViacomCBS, a mysterious character with a dubious ethical track record had convinced many of the largest and most prestigious banks in the world, including Goldman Sachs, Nomura, Credit Suisse, UBS, and the aforementioned Morgan Stanley, to use their balance sheets to help him effectively amass a huge stake in the company while simultaneously circumventing reporting rules established by the US Securities and Exchange Commission (SEC). Bill Hwang, founder of the family office Archegos Capital, entered into swap agreements with these banks with which he assumed the economic risk associated with the movements of several stocks without formally owning the shares himself. By some estimates, Hwang synthetically owned more than 20% of ViacomCBS and similarly outsized economic stakes in Discovery, Baidu, Tencent Music Entertainment, Vipshop Holdings, Farfetch, and GSX Techedu.

Hwang was running this scheme at such a large scale that he was effectively bidding up his own book, creating what Nassim Taleb would call a self-licking lollipop. While the full story of Hwang’s collapse is yet to be told, it seems as though China’s unexpected crackdown on internet and online education companies caused some of Hwang’s holdings to tank, creating a cascading series of margin calls that he could not meet. ViacomCBS’s ill-timed raise was the grain of sand that grew into an avalanche of losses that ultimately measured over $10 billion. We let the New York Times take it from here (emphasis added throughout):

“By Thursday, March 25, Archegos was in critical condition. ViacomCBS's plummeting stock price was setting off ‘margin calls,’ or demands for additional cash or assets, from its prime brokers that the firm couldn’t fully meet. Hoping to buy time, Archegos called a meeting with its lenders, asking for patience as it unloaded assets quietly, a person close to the firm said.

Those hopes were dashed. Sensing imminent failure, Goldman began selling Archegos’s assets the next morning, followed by Morgan Stanley, to recoup their money. Other banks soon followed.”

Setting aside the potential anti-trust issues involved with the meeting called by Archegos, or the comically-predictable development that Goldman Sachs stabbed everybody else on the call in the back by rushing to the exit first (surprise!), or the fact that Morgan Stanley quickly followed suit and flushed large blocks of stock in a company it had just served as lead book runner for, the entire tawdry affair raises many serious questions. Where are the regulators? Why do our largest, most well-resourced banks demonstrate absolute incompetence in risk management and compliance? A year on, why is Bill Hwang still a free man? How were so many bankers, all trained to know better, intent on picking up nickels in front of the Archegos steamroller? Surely, lessons have been learned, right?

Nope.

For the latest speculation-fueled folly in market breakdowns, we turn to the historic events unfolding in the nickel market. As has been widely reported, the price of nickel soared to unimaginable heights last week on the back of an epic short squeeze. Xiang Guangda, the self-proclaimed “Mr. Big Shot” of the nickel market and owner of Tsingshan Holding Group Co. (the largest nickel producer in the world), made a massive bet against the price of nickel prior to Russia’s invasion of Ukraine, and that bet turned against him, badly. Here’s how Bloomberg describes the situation:

“JPMorgan Chase & Co. is the largest counterparty to the nickel trades of the Chinese tycoon caught in an unprecedented short squeeze, putting the bank at the center of one of the most dramatic moments in metals market history.

About 50,000 tons of Xiang Guangda’s total nickel short position of over 150,000 tons is held through an over-the-counter position with JPMorgan, according to people familiar with the matter. Based on that figure, the tycoon’s company, Tsingshan Holding Group Co., would have owed JPMorgan about $1 billion in margin on Monday. The nickel producer has been struggling to pay margin calls to its banks and brokers, Bloomberg reported this week.

JPMorgan is leading discussions between Xiang and roughly 10 banks and brokers through which his nickel short position is held, the people said, asking not to be identified as the talks are private.”

In reaction, the London Metal Exchange (LME) took the unprecedented step of retroactively canceling vast swaths of trades as the price of nickel kept rocketing higher. The significance of this decision will continue to reverberate for many years, and we believe it could catalyze the end of the LME itself. Here’s how London-based Financial News explained the move:

“Nickel traders were blindsided this week as the wild ride in the metal saw prices more than double in overnight trading – prompting the London Metal Exchange to cancel orders and halt trading.

Nickel trading on the LME still hasn’t resumed, and the halt will likely extend until at least mid-March as the exchange weighs its options. The sudden suspension affected an estimated 9,000 trades worth $4bn.

Canceling the trades helped Tsingshan Holding Group. The China-based stainless steel producer is estimated to have lost $8bn on its short position. Because the LME canceled trades, Tsingshan losses are potentially less severe than if the trades had stood. The holding group’s chair, Xiang Guangda, is reportedly still holding short positions on nickel.”

Of course, if the moves by the LME help Tsingshan – and by extension their banking counterparties – they must hurt other investors. There are two sides to every trade, after all. While we are not experts in the nuanced mechanics of how the LME functions in practice, it requires no special knowledge to deduce that if the normal default waterfall had been allowed to occur, the very existence of the LME would have been threatened. Undoubtedly, the LME’s desperation was inversely proportional to its effective solvency, as the robustness of their default management plan would have been sorely tested.

For confirmation, we turn to someone who does have such expertise, namely Russell Clark. Clark has been blogging about the risks posed by clearinghouses for some time at his Substack, Capital Flows and Asset Management. In a piece published last week called What’s Happening with the LME and Nickel, Clark used a video presentation to walk through the events and their likely consequences. Here’s a quote that stood out to us:

“For me, the clearinghouse looks (like) a broken financial institution… They’ve gone from being a shock absorber to now a propagator of risk.”

Yesterday, JPMorgan cut a standstill agreement with Tsingshan and the LME hopes to reopen nickel trading tomorrow. The LME also announced 15% daily limit moves across all metals. However things play out from here, we believe the LME is functionally finished. Trust was their bond, and they defaulted on it last week.

Back in October of 2021, we wrote a piece called Dr. Copper is Sick, in which we chronicled a similar set of circumstances that unfolded at the LME in the copper market, albeit on a much smaller scale. Still, the behavior of the LME surprised many market participants, and can now be viewed as an ominous foreshadowing. Here’s how we closed that article:

“More importantly, the LME damaged its credibility in the marketplace. It either facilitates price discovery and thereby serves a useful purpose, or it doesn’t. Apparently, it doesn’t.

Attempts to suppress price inevitably cause product shortages and higher prices down the road, and we expect this time to be no different. If a well-run physical exchange facilitates lower prices and assures ample supplies, surely a broken exchange does the opposite.”

Russia’s invasion of Ukraine was sure to kick off a chaotic series of unpredictable and historic moves in the global financial markets. The functional death of the iconic London Metal Exchange is but the first of what we expect will be many similarly situated institutions to get sucked under the steamroller.

RIP LME.

If you enjoy reading Doomberg, please do us the HUGE favor of simply pressing the “Like” button.

Excellent analysis. One can go further and point to the eviction moratorium and the freezing of protestors’ bank accounts as ominous signs of the willingness of governments to set aside contract law and to act without due legal process, with no opportunity for the parties involved to defend themselves.

You may not care about landlords or agree with Canadian truckers: you should be concerned about the precedent that has been set.

Business in the west has been underpinned by confidence in the rule of law and financial institutions. Once that disappears, the incentive to take on business risk goes, too.

You used to say that when you completely trusted someone’s credentials you could, “take it to the bank.” Now that saying is laughable.

To sit back and see Pfizer withdraw EUAs, Biden try to shove the energy blame to Putin, Trudeau using emergency measures and continuing to keep the Canadian border closed to unvaccinated travelers leaving, the CDC hiding data and banks doing what they did in 2008 yielding the symptom such as the failure of the LME… it begs the question as to how many shoes need to drop until the system is fully rebuilt on honesty and transparency and criminal charges for breaking the law.