Reflections from the Lake

“Inflation is everywhere and always a monetary phenomenon” – Milton Friedman

I happen to slightly disagree with Mr. Friedman, but more on that later…

I’m in the lumber business by accident, you see. Three years ago, my good friend Bob pitched me on investing in a partnership he was putting together. Bob is passionate about land. Rural land, in particular. The concept was simple: buy expansive acreage of affordable land in flyover country, harvest a good chunk of the available lumber and gravel, clean up the property, and sell it in a year or two for a tidy profit. Mix in a bit of leverage and we could easily achieve a 15-20% annual return on equity with minimal risk, likely more.

We won’t get rich this way, I thought, but it sure beats keeping cash in a bank account, and I don’t trust the stock market. Besides, I’m always experimenting with businesses and I value the ability to learn new things, so I took the plunge.

The business has largely worked as advertised (especially this year!). Along the way, I began to personally fall in love with the concept of owning some land myself. A nice hedge against inflation, I figured. Besides, that’s what middle-aged people do. I asked Bob to keep on the lookout for a nice property, relatively close to where I live, with some lake frontage. In December I got the call.

“I found the perfect property for you,” Bob said. And boy was he right. Rolling hills, soaring soft maples, plenty of lake frontage, miles of walking trails, and less than an hour from my home. It was, in fact, perfect. Within a week of that call, I had the property under contract. We closed shortly after the new year.

As spring arrived, I decided it was time to level up my lake game – I needed an all-terrain vehicle to get around my property. I stopped by my local Polaris dealer and was surprised by what I found. Minimal inventory, empty showroom space, and a somewhat apologetic saleswoman.

“We have these two over here, one for $32k and the other for $34k, and they won’t be here for long,” she said with a shrug.

$32k for an all-terrain vehicle? Sure, it looked nice and had four seats, but I had mentally budgeted about $10k. I asked about when they would get more inventory of some of the more affordable options, and she demurred.

“Not for several months at least – chip shortage.”

I had seen many references to the chip shortage in the auto sector on Twitter, but it was a little jarring to be confronted with it so directly in a loosely related market. I certainly wasn’t going to spend $32k on an ATV for the lake. I needed another plan.

Golf carts! I figured a gas-powered golf cart would do the trick. Probably a safer option for my kids anyway, and surely I could find one of those. I did some research and found a dealer 30 miles away. A nice lady picked up the phone when I called.

“We won’t have any new models until July at the earliest because of the chip shortage. We do have two used Yamahas avail-”

“I’ll be there first thing tomorrow,” I interrupted.

Without bothering to negotiate, I paid the full asking price of $6,500 and became the proud owner of a souped-up 2016 Yamaha golf cart. I don’t even know how many miles it has on it. There were only two choices, so I simply picked the color I preferred and handed over my credit card.

“Our family has been in the golf cart business for 40 years and I’ve never seen anything quite like this,” she said as she filled out my paperwork.

I don’t own a pickup truck, so I had to arrange delivery directly to the lake. She was happy to oblige, for a fee of course. Maybe I should get a pickup truck, I thought to myself. I’ll probably be hauling things back and forth to the lake.

I decided to do some research on pickups. Hmmm. My local Ford dealer has precisely three new F150s in stock. Odd. They usually have 40-50 on the lot. I bet it’s that damn chip shortage again. The Toyota Tundra is nice. My local Toyota dealer had a few more of those. Interestingly, they had some used Tundras in stock as well. Maybe I’d get a better deal buying used.

Huh. A brand-new Tundra for $50k. Pricey, but in this market, I’m just glad they had some stock to choose from. Oddly, a similarly-equipped 2018 Tundra with 20,000 miles on it is listed for $44k – something is up in the used car market. At that price, why wouldn’t I just buy new? I guess if there’s not much new to choose from… feels like new car prices are likely to go up, and soon.

I punted on the pickup decision for now, figuring I would first get a sense of how much lumber I could harvest from the lake property. Bob arranged for me to meet our lumber guy, Dan, at the lake the next morning.

“I walked this property with Bob back in December. You got an amazing deal. I bet you could flip it today for a 40 percent gain,” Dan said.

A 40 percent gain in only four months? That can’t be right. Sure enough, I later dug into the spring land transactions in the surrounding counties. Prices have exploded. Not only that, Dan estimated that if we only took down the largest trees (those with a diameter of 18” or more), we could preserve the beauty of the property, allow the existing younger trees to flourish, AND generate enough revenue to cover HALF the price I paid for the land back in December.

“Lumber prices are crazy. I’ve never been busier,” Dan said, as he systematically spray-painted a dot on each of the trees he’d be removing in a few weeks.

At dinner that evening, I began to retell part of this story to my family, only to have my teenage daughter interrupt me to explain how she already knew all of this from TikTok. Apparently, lumber-as-the-new-gold memes and videos had been circulating on the platform for weeks.

I chewed over all these events as I chewed on my freshly-grilled steak, itself much more expensive than before Covid. Now about that pickup truck, I thought to myself…

Despite their high-tech sounding name, semiconductors chips are, in fact, highly commoditized products with all the hallmarks of a boom/bust business: long lead times for expensive production capital, hesitancy on the part of incumbents to invest until the very worst moment, after which they over-invest together, standardized products built to specifications, wide use across multiple industries, and highly sensitive price elasticity of demand. In short, there’s not much difference between semiconductors and oil or polyethylene.

Why is there a worldwide shortage of chips today? Echoes of the Covid shutdown, primarily, plus a healthy dose of fear of missing out (FOMO) on the part of procurement teams globally. By echoes of the Covid shutdown I mean that things came to a screeching halt in early 2020 and disrupted capital spending plans in virtually all asset-heavy businesses. The demand forecast for commodity goods did a historical 180-degree swing, from the world is ending (crashing demand forecasts) to the panic ordering we see today (and hoarding of limited supplies). One only needs to inspect the price of crude oil for evidence of the whipsaw…

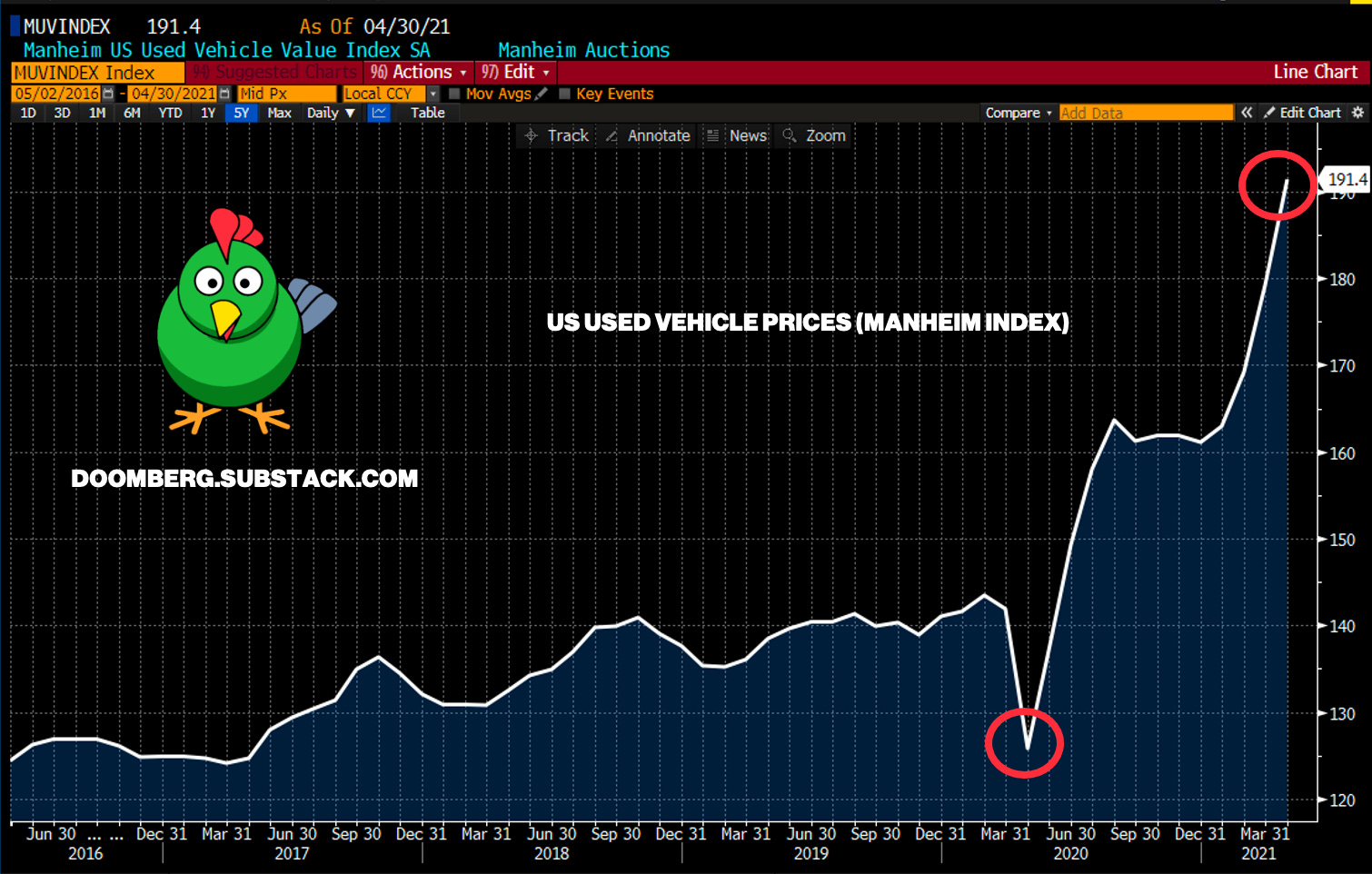

…or the price of used cars…

… to get a jarringly direct view of the impact of the chip shortage.

Another factor that is currently stressing supply chains is the pre-Covid years of under-investment in maintenance capital. During tough times, firms respond by putting off needed investment that becomes critical once demand reappears. When you crank your factory back to high, things break. The recent foundry fires have turned a serious problem with semiconductor supply into a full-blown crisis. It will probably get a lot worse before it gets better – you can’t flip a switch and build a foundry. Similarly, we are witnessing a very muted production response to rising oil prices in the US shale patch. Responding to price signals takes time in heavy-asset industries. These are big battle ships that don’t turn on a dime.

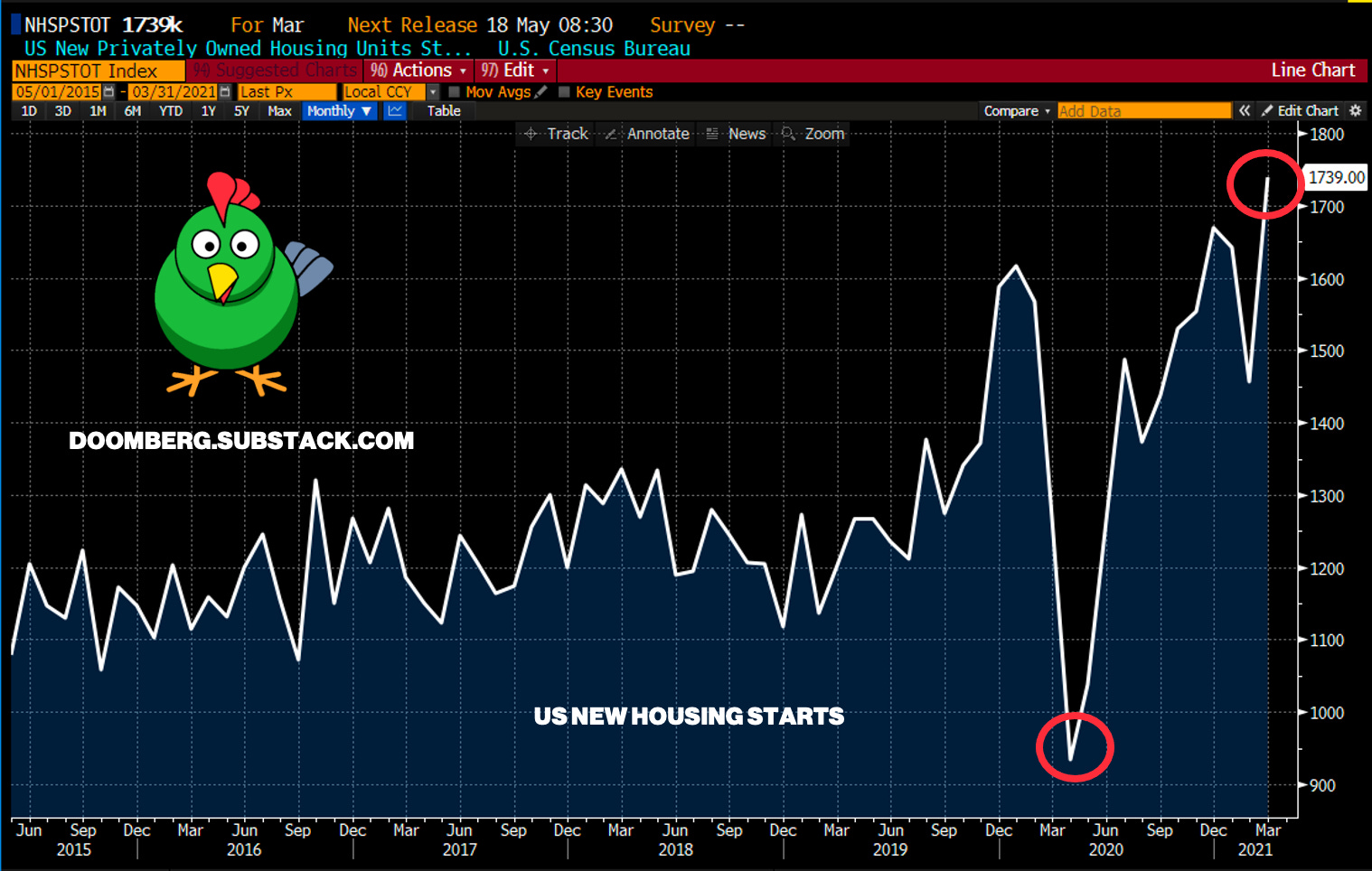

It is the same story with lumber, of course, as mill operators and lumber dealers completely misread the impact of Covid. Demand for housing, spurred by crashing mortgage interest rates and an unprecedented wave of relocations out of the cities has sparked an unanticipated home building boom…

…and lumber prices going totally vertical.

Almost all key economic inputs are levitating. Take copper, as an example. Or zinc. Or polyethlene. Everywhere I look, I see heavy industry unable to keep up with newfound demand. The saying goes that the cure for high prices is high prices. The investment cycle will play out, industry will respond, new supply will come online, and prices will eventually swoon. That’s certainly the position of the Fed, which is actively cheering on inflation and is doing its best to convince the world these price hikes are healthy and transitory. They certainly could be.

However, I believe we are experiencing a convergence of three forces unprecedented in our history. These are (1) a combination of extreme easing of BOTH monetary and fiscal policy, (2) huge supply chain hiccups globally, and most unique to today, (3) an interconnected global zeitgeist shaped (controlled?) by social media via viral videos, memes and other dopamine-inducing tools. This last point is critical. Inflation is fueled by FOMO – people assume the today’s price is worth paying, no matter how high, because they KNOW it is going higher tomorrow. We’ve never experienced a bout of inflation in the era of TikTok, Twitter, Instagram and Facebook. What happens when a TikTok video of the first $20 Big Mac goes super viral?

What causes a period of elevated inflation to transform into outright hyperinflation? Historically, it coincides with a complete collapse in the confidence of a country’s currency. Confidence is, of course, a psychological state of mind. Our minds have never been more vulnerable to manipulation. I would argue that the path from elevated to hyper is a lot shorter than our leaders think. I would further stipulate that Chairman Powell probably doesn’t spend much time on TikTok. We are running a dangerous experiment. Time will tell.

Back to Mr. Friedman. I believe inflation is always and everywhere a psychological reaction to a monetary phenomenon. I’ll be buying that pickup truck next week, because I KNOW prices will only be going higher the week after. My FOMO is real, and I suspect I’m not alone, just early.

If you enjoy Doomberg, email a link to this piece to your most paranoid friend.

It's funny, the very moment I finished reading When Money Dies, my first thought was, welp... That's a book I'm gonna need to be reading again.

Hey Doomberg, if you had the ear of RFK Jr. and suggest he interview one person to shift his view of nuclear power, who would that be? Other than yourself...I mean, he might interview a green chicken, but a live human expert might be more influential. Thanks!