Sitting Down With Sprott

“There is no substitute for face-to-face reporting and research.” – Thomas Friedman

Late 2021 and early 2022 will undoubtedly be remembered for the tectonic shifts in geopolitics that flowed directly from a crisis in energy. What started as a shortage of natural gas in Europe spread quickly to Asia, and ultimately evolved into an ongoing inflationary spiral for most of the critical inputs that drive our economy. As is all too predictable in such circumstances, military conflict has broken out, and one hopes conflict contagion can be prevented.

Nothing focuses the mind like a crisis, and no technology is poised to benefit more from our inevitable reconciliation with physics than nuclear energy. The early signs of a sober reconsideration of the policy errors that got us in this predicament are finally emerging. Recently, British Prime Minister Boris Johnson completed a near about-face on the topic, lending the full weight of his position in support of a nuclear renaissance:

“Boris Johnson has told nuclear industry bosses that the government wants the UK to get 25% of its electricity from nuclear power, in a move that would signal a significant shift in the country’s energy mix.

Johnson on Monday met executives from major nuclear utilities and technology companies including the UK’s Rolls-Royce, France’s EDF, and the US’s Westinghouse and Bechtel to discuss ways of helping to speed up the development of new nuclear power stations.”

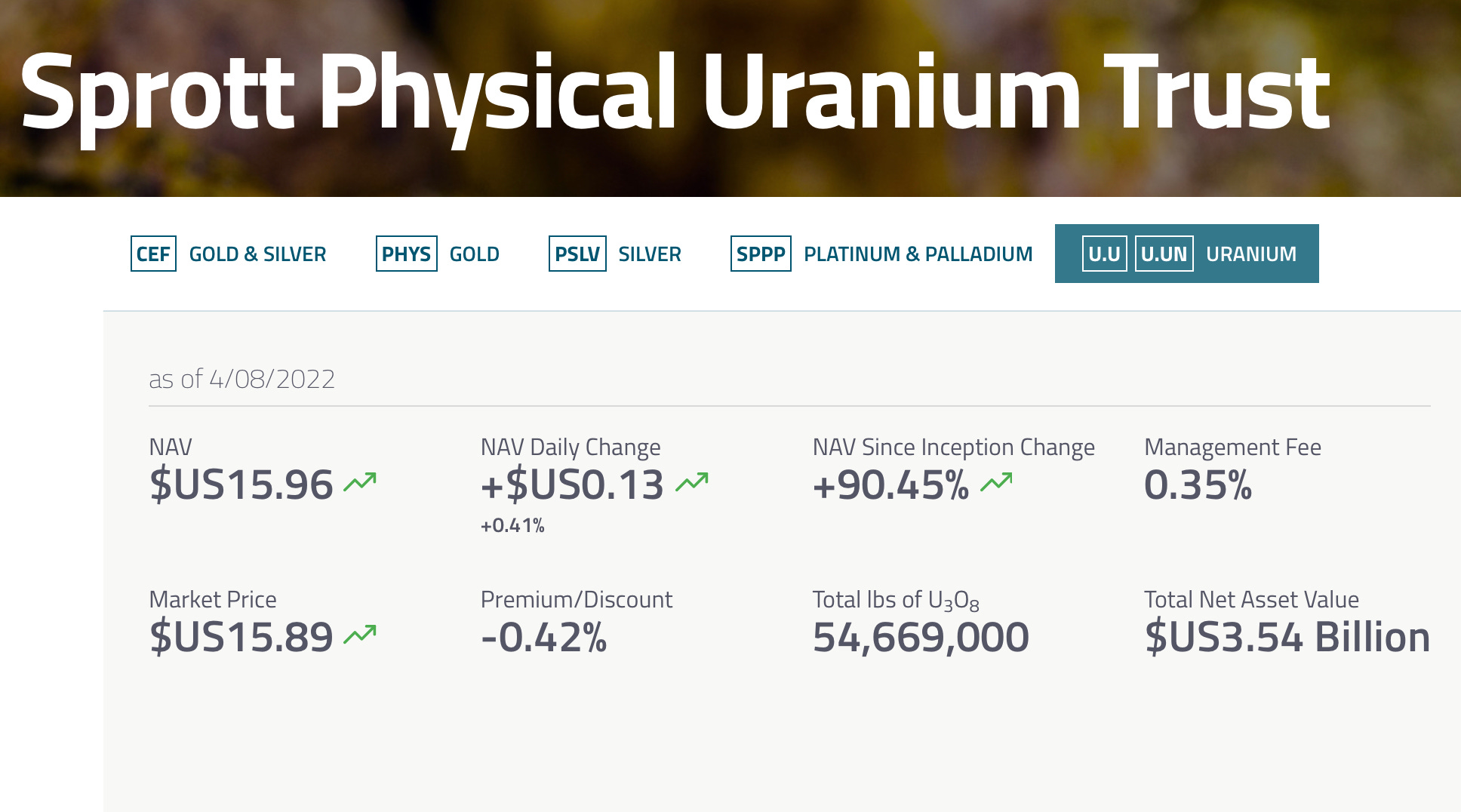

In parallel and coincident with these developments, a financial revolution is underway in the market for uranium, the fuel that powers nuclear energy reactors. (In September, we wrote about the significant changes occurring in that market here). By acquiring Uranium Participation Corporation (UPC) and reorganizing it into the Sprott Physical Uranium Trust (SPUT), Sprott Asset Management has set about the task of bringing order and transparent price discovery to the market for uranium. Judging by the events that have unfolded since they embarked on this mission, their timing has been impeccable. The price of Uranium has doubled, SPUT continues to buy and sequester millions of pounds of uranium, the price of many uranium mining stocks has soared, and interest in nuclear power as the ultimate form of green energy is growing.

A few weeks ago, we made an appearance on Antonio Atanasov’s podcast Resource Talks to give an update on our uranium views (you can follow Atanasov on Twitter here, and listen to the uranium portion of our appearance on YouTube here). Shortly after that published, we met John Ciampaglia, CEO of Sprott Asset Management, over email. We had been keenly interested to learn the mechanics of how SPUT actually works and what Sprott’s long-term intentions are with that vehicle and asked if he would sit down with us for an interview. Ciampaglia obliged, and what follows are highlights from that wide-ranging discussion, lightly edited for readability.

Disclosure: Members of the Doomberg team are long SPUT, which trades in the US under the symbol $SRUUF and on the Toronto Stock Exchange under the symbol $U_U. We consider ourselves long-term holders and do not intend to change our position anytime soon. Nothing in this article should be considered investment advice.

We began by asking Ciampaglia how SPUT raises money and how it procures uranium. There is some confusion on Twitter about whether SPUT needs to be trading at a premium to its net asset value (NAV) before it can issue new shares. Ciampaglia’s answer clarified things nicely (emphasis added throughout):

“The program is called an at-the-market offering (ATM), and essentially how that works is we have two underwriters, Vertu and Cantor Fitzgerald, both in the United States, and they act as the underwriters for the at-the-market program. The test is fairly simple. If the trust is trading at a higher value than the previous day’s net asset value (NAV), it gives us the ability to issue new units throughout the day. And as an investor, you may buy some shares and you have no idea whether you happened to buy an existing share that was trading on a secondary basis, or you were going to receive a newly minted treasury share that the underwriter sold you, and at the end of the day comes to us and says, ‘I sold 228,000 new units today. Please give them to me because I'm short, so I can settle all my trades.’ And they give us the net cash, and we take that net cash, and we buy more physical uranium.”

“We completely control the ATM. The underwriters do not. We will send them instructions over the course of the day around where we want them to issue shares, be more aggressive, pull back, turn it off, turn it on. It's a really good tool, and I think the marketplace, once they figure out how it works, has responded accordingly. Because I think since August 17th, when we initiated the ATM, we've now raised about $1.65 billion through it. So, fast forward the trust, $630 million in July, and I think we hit $3.2 billion AUM as of last night.”

There is similar confusion related to how and when SPUT buys its uranium and whether the question of premium or discount to NAV is a factor in that decision. Turns out the answer is no:

“In terms of us buying uranium, that is a separate decision. Once the cash is raised, we will start immediately looking for pounds. For example, if we were issuing new units this morning, we will literally concurrently be looking to place the capital even before the trades settle, because I know I'll get the cash on T-plus two, but I'll go buy uranium with a T-plus 30 settlement period. Right? So, on days where we're really active with the ATM, we're shopping, basically, all day looking for uranium.

The premium and discount don’t have any bearing on our buying program. Once the cash is in the fund, then our job is to survey the market, find the best available offers. We're not beholden to any one producer. We've purchased uranium from 25 different counterparties so far. And so, we cast the wide net, we talk to people all around the world. It's not an easy product to buy. There's a lot of different time zones. We're often trying to get ahold of people before they go to bed in Asia. It's a lot of manual work.”

Building on the discussion about NAV, we asked Ciampaglia whether he worries about the fact that SPUT is a closed-end fund (meaning shares are not redeemable). Typically, closed-end funds can trade at a significant discount to NAV. His answer was illuminating:

“Closed-end funds obviously will trade at premiums and discounts to NAV. It's one of their, I would say, their limitations relative to the open-ended ETF structure which, historically, those funds will trade very close to NAV because there is a daily arbitrage mechanism built into those structures. With a closed-end fund, we control the basic supply of shares in the marketplace through the ATM, so that's something that closed-end funds historically don't do. They don't typically raise capital after they initially IPO because, as you mentioned, they historically trade at discounts. But when you look at the Sprott Physical Bullion Trusts, and you look at the Physical Uranium Trust, what you'll notice is that they generally will trade in a pretty tight collar to their net asset value. And that's because we market the funds constantly. We have a very loyal shareholder base, and there's different types of investors that will help arb away any discount if it persists.”

“One of the structural changes we made to Uranium Participation Corp to help mitigate that risk is we calculated the net asset value every night. And this is the first of its kind. The predecessor vehicle would publish a net asset value once a month. When you think about a commodity as opaque as uranium, I often joke with people that it's almost impossible to find a price on a screen for uranium unless you have professional services, or you have a subscription to one of the pricing reporters. It's really hard to even find a price.

If you're not providing transparency to your shareholders around what the net asset value is on a very frequent basis, and you have an opaque uranium price to begin with, it doesn't give investors the tools or the information to know exactly where the fund is trading and how they should be buying and selling it. And I think our hope is that our trust will trade in a much tighter collar versus the predecessor vehicle, or for that matter, Yellowcake [Yellow Cake PLC, OTCMKTS, Symbol: $YLLXF] right now, which is trading at a 7% or 8% discount to its value, even though it only publishes a NAV once a month.”

Although SPUT does trade on the main stock market in Canada, it only trades over-the-counter (OTC) in the US, which can limit the profile of investors who can participate in the trust. A key objective of the Sprott team is to upgrade SPUT’s listing to the New York Stock Exchange (NYSE), something many uranium investors are anxiously awaiting. We asked Ciampaglia whether he could give our readers an update on the topic:

“… the last piece of the puzzle of our program is to pursue a New York Stock Exchange listing, which we think will be the cherry on top. I think the marketplace has figured out that we've been able to do an enormous amount of good in the marketplace, just with the TSX listing. It's going to be a bit of a battle working through the SEC review process, but it's something we're committed to, something we're paying for out of pocket. And we're very close to actually making that filing. The NYSE just emailed me this morning saying, they're putting the finishing touches on it. So, we hope in the next few weeks, you'll see at least a receipt on New York Stock Exchange website that the filing has been made to the SEC.”

Sprott Asset Management made news several months ago when it announced its intent to acquire the North Shore Global Uranium Mining ETF (NYSE Arca, Symbol: $URNM) and reorganize it into the Sprott Uranium Miners ETF. On the day we interviewed Ciampaglia, it became clear that shareholders would approve the deal, and we asked him about his plans for the URNM franchise. His answer lays bare just how small the overall market for uranium mining stocks is compared to other commodities, which he sees as defining the opportunity for future growth:

“We are hoping that on or about April 25th, the fund reorganization will be complete, and it will add another uranium product to our suite. We're very excited about it. We think it's the best index in terms of its pure play to the uranium miners. I think Tim Rotolo, the current sponsor, has done an incredible job growing that thing from nothing to over a billion dollars. I just finished a call with my sales team, and they asked me a question about what's some of the biggest objections you think you're going to get about the ETF? And amazingly what we find is it comes down to investability. And what I mean by that is we talked to a lot of institutional investors who said, ‘We've done all this work on uranium. We really love the thesis. It's really great. Now we want to allocate capital, and there's three or four things we're able to buy because the sector's so small.’

And it's like, ‘Wow, that is really telling.’ And look, that's a byproduct of a nine year bear market where hundreds of companies disappeared, capital was washed out, and now money's trying to come back and they say to us, ‘Okay, your fund is pretty big, so that's interesting to us, but beyond one or two producers it's really hard to get invested in these companies.’ And I use this example in a presentation. I say, ‘Look, we did a study and there's about 80 odd publicly traded uranium companies, and the combined market cap of all 80 companies is about $37 billion.’ Exxon is 10 times that.

When you think about these companies producing a critical mineral that happens to generate 10% of the world's electricity, it is pretty mind-boggling that the collective value of them is only $37 billion. Even if you compare it to some smaller companies, some smaller oil and gas companies, those companies are still two times the combined market cap of these 80 uranium stocks. We think there's a lot of room. Even though the stocks have moved, we still think there's a lot of room for them to run as they get recapitalized, and they finally get projects back online that have been mothballed for years.”

The third-largest holding of URNM is SPUT itself, which could present a conflict of interest. We asked Ciampaglia how Sprott Asset Management intended to handle this situation:

“We will be the sponsor of the ETF and the ETF will license the index from North Shore Indices, and that's Tim Rotolo's company. We want to be arm's length from Tim. We like his index design. We like what he's done, so we wanted to continue that. It’s really his decision if he was going to adjust the index methodology at any time in the future. We'd rather not be involved because of the conflict. We think SPUT being a material holding in there adds a lot of liquidity and diversification against some of the more volatile miners, so we think it makes great sense. But in terms of what the end weight is, that's really up to him and his index methodology.”

Note: The full transcript of our conversation with Ciampaglia – including his reaction to the AMC/Hycroft Mining deal and the mechanics of physical redemption in PHYS and PSLV – as well as our thoughts on the potential investment consequences of the consummation of the URNM deal, will be emailed to Doomberg Pro members tomorrow, Sunday, April 10th.

What is clear from our time with Ciampaglia is this: Sprott Asset Management is committed to professionalizing the uranium investment landscape. They intend to offer better investment vehicles with enhanced optionality and liquidity than has ever existed in the space. We suspect all members of the sector will benefit from these efforts.

While no investment is without risk – the uranium industry is always one low-probability nuclear accident away from a severe bear market, after all – we came away excited about the long-term prospects for uranium. We reiterate the need for readers to do their own due diligence before making investment decisions.

We close with a reminder that Doomberg is now open to paying subscribers and we will officially pivot to a paid newsletter after April 30. We’re keeping a spot warm for you in the Chicken Coop – upgrade today!

Off topic, but Sprott is still firing people for not taking the jab - disgraceful.

Did you guys notice Russia displaying to the world the vulnerability of having nuclear power plants as wartime potential shields/targets in Ukraine? That was not subtle or unintentional. That will remain as an existential issue and threat to nuclear power going forward. We’re seeing that former rules based tactics of war are off the table with US confiscation of Sovereign reserves, Hypersonic missiles, threats of Nukes, Killer drones, Cyber warfare, etc….Nothing is off the table and game theory favors unintended consequences and therefore the unthinkable is no more.