Magnesium, P.I.

“The reactions of organic magnesium compounds are of two kinds – reactions of substitution and reactions of addition.” – Victor Grignard

On September 8, 1998, a tropical depression formed over the Western Gulf of Mexico that eventually became Tropical Storm Frances. Three days later, it made landfall just north of Corpus Christi and left significant flood damage in its wake, especially to the east which took the brunt of the storm surge and rainfall. Brazoria County, home to several critically important petrochemical complexes, received anywhere from 8-16 inches of rain.

Although Frances was undoubtedly a powerful rainmaker, from a meteorological perspective there wasn’t much about the storm that made it historically significant – certainly not compared to Hurricanes Katrina and Rita or Tropical Storm Harvey. Our interest in the event stems from the fact that you can trace the terminal decline of America’s leadership in – and China’s subsequent domination of – magnesium production to the fallout from Frances. Magnesium is yet another critical-to-the-global-economy input that is no longer within the West’s control.

For the better part of 80 years, Dow Chemical was the world’s primary producer of magnesium. Its sprawling petrochemical facility in Freeport, Texas was constructed as part of America’s manufacturing ramp-up during World War II. Because magnesium can be converted into strong-but-lightweight alloys, it was put to good use in the production of military aircraft. In support of the Allied war effort, Dow built a huge magnesium plant within its Freeport site, using seawater and electricity to make the metal in purified form.

Making magnesium from seawater is incredibly energy intense and creates significant environmental challenges. Already struggling with poor profitability, growing competition, and significant reinvestment needs, flood damage from Tropical Storm Frances was the final straw for Dow. The company initially declared force majeure in the aftermath of the storm and exited the magnesium business entirely a few months later.

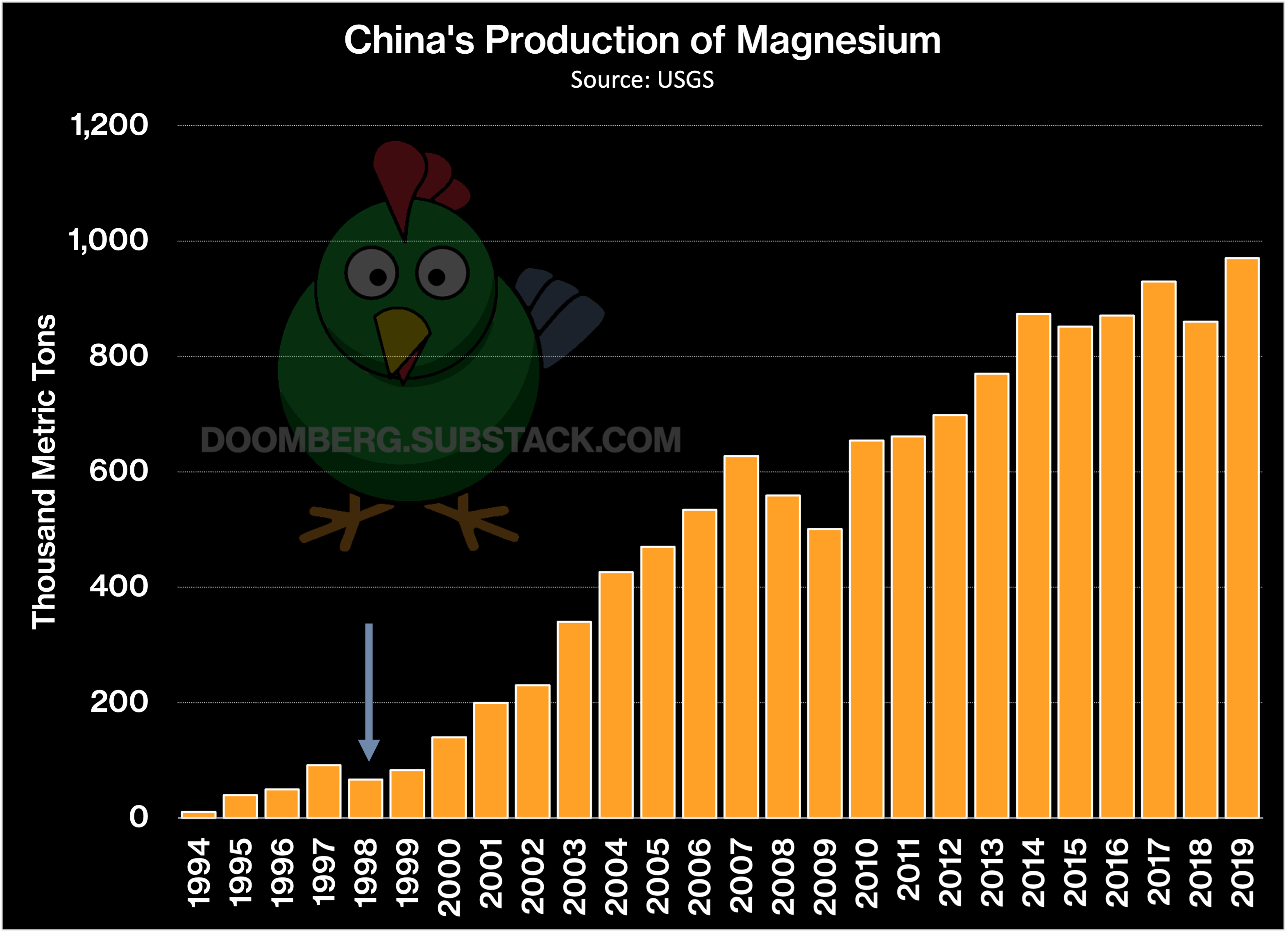

In the years immediately prior to Dow’s exit in 1998, the US produced about half of the world’s magnesium. Today, the one remaining plant in the country is operated by US Magnesium, LLC near Salt Lake City, Utah, and captures only ~5% global market share. That facility has long been a key target for shutdown by environmentalists because of its worker safety and pollution issues. Earlier this year, the company entered into a comprehensive settlement with the EPA in an effort to resolve alleged illegal disposal of hazardous waste:

“The U.S. Environmental Protection Agency (EPA) and the U.S. Department of Justice (DOJ) today announced a settlement with U.S Magnesium (USM) to resolve violations of the Resource Conservation and Recovery Act (RCRA) and require response actions under the Comprehensive Environmental Response, Compensation and Liability Act (CERCLA) at its Rowley, Utah facility. The settlement includes extensive process modifications at the facility that will reduce the environmental impacts from its production operations and will ensure greater protection for its workers.”

Ironically, Dow’s exit from the magnesium market began just as demand for the metal started to skyrocket. One of the main uses for magnesium is in the production of aluminum alloys, a strong and lightweight material that has allowed automakers to meet ever-increasing fuel economy standards. By replacing parts traditionally made with steel, automakers have shed hundreds of pounds from passenger vehicles with no meaningful sacrifice to structural integrity. When it comes to fuel economy, every pound counts, and aluminum alloys appear in many components of modern cars, including body panels, gearboxes, cargo beds, and seat frames.

According to the United States Geological Survey (USGS), China now produces roughly 85% of the global magnesium supply. Taking advantage open access to cheap coal, China used what’s known as the Pidgeon Process to flood the world with subsidized magnesium, causing traditional producers to throw in the towel. Norway’s Norsk Hydro closed its domestic magnesium facility in 2001 and its plant in Quebec, Canada in 2006. France’s Pechiney exited the business in 2002. Today, in addition to US Magnesium’s Utah plant, there exists some production in Russia, and a scattering of smaller facilities in Kazakhstan, Israel, Brazil, Turkey, and Ukraine. China’s domination of the industry is thorough.

In a pattern that will come as no surprise to regular Doomberg readers, the energy crisis that started in Europe has spread into China, and authorities there have taken draconian steps to curtail industries that require substantial energy to operate. We’ve previously described the impact on the production of polysilicon, a market that experienced a similar assault by China in the past few decades. China’s response to the current energy crisis is leading to a supply shock in the solar industry, reversing years of cost improvements. It’s a similar story with magnesium, only the potential impact on the global economy is substantially higher (emphasis added):

“Europe’s industry associations European Aluminium, Eurofer, ACEA, Eurometaux, industriAll Europe, ECCA, ESTAL, IMA, EUWA, EuroAlliages, CLEPA and Metals Packaging Europe have today issued an urgent call for action against the imminent risk of Europe-wide production shutdowns as a consequence of a critical shortage in the supply of magnesium from China.

Magnesium is a key alloying material and widely used in the metals-producing industry. Without urgent action by the European Union, this issue, if not resolved, threatens thousands of businesses across Europe, their entire supply chains and the millions of jobs that rely on them.

Due to the Chinese Government’s effort to curb domestic power consumption, supply of magnesium originating from China has either been halted or reduced drastically since September 2021, resulting in an international supply crisis of unprecedented magnitude.

With the European Union almost totally dependent on China (at 95%) for its magnesium supply needs, the European aluminium, iron and steel producing and using industries together with their raw materials suppliers are particularly impacted, with far-reaching ramifications on entire European Union value chains, including key end-use sectors such as automotive, construction and packaging.”

When a stone is dropped into a pool of water, the ripples emanate from its point of entry outward in concentric circles. Energy is the lifeblood at the center of the economy, and so it is only natural that the explosions we are observing in the price of energy in Europe and Asia will make their way outward through the many value chains of manufacturing. Since the production of magnesium is so energy intense, its price chart mirrors that of liquified natural gas, fertilizer, polysilicon, and the many others crossing our terminal today. These cost pressures will soon be passed on to chemicals, food, solar panels, and cars, adding further fuel to the inflationary fires igniting across the globe.

When we eventually emerge from the energy crisis, the story of how China came to dominate the magnesium market should inform a strategic reconsideration of the West’s entire approach to the economy. Certain critical raw materials are difficult to make and doing so with all appropriate environmental controls is a price worth paying. Allowing China to abuse its environment so it can flood the world with cheap goods and put our manufacturers at a terminal disadvantage is dumb policy.

We need to get smarter, and soon.

If you enjoy Doomberg, subscribe and share a link with your most paranoid friend!

Great read Chicken...how long did it take you to decide if the mustache goes above or below the beak?..

Doomberg, I'd be interested in seeing a thorough and thought out writing from the team on how to handle some of these topics on a policy level - state subsidies, tariffs, etc. It seems that the policies of both political parties are designed to war against each other for maximum failure; unions raise labor costs without the focus on actually producing goods, while the "free market" religious mantra almost always assures that we'll be undercut by states and locals with lower living standards, lower environmental standards, willing to state subsidize, and/or willing to engage in currency manipulation.

Obviously, its a complicated topic! One worthy of the Doomberg team!