This Year in Gas

A look back at the most interesting energy market of 2024.

“Does anyone here read the energy analyst Doomberg?” – Australian Senator Matthew Canavan

To understand energy markets, one need only internalize four things. First, energy is life—a point so central to our framework of macroeconomic and geopolitical analysis that it needs no further elaboration in today’s pages. Second, energy is fungible, and all primary forms of energy, being additive to the human endeavor, will be greedily consumed in its pursuit. Third, energy prices are highly inelastic, such that mere percentage points of regional supply imbalances cause wild market swings. Finally, the energy industry is reliably incapable of self-discipline, unable to resist the allure of drilling the next well.

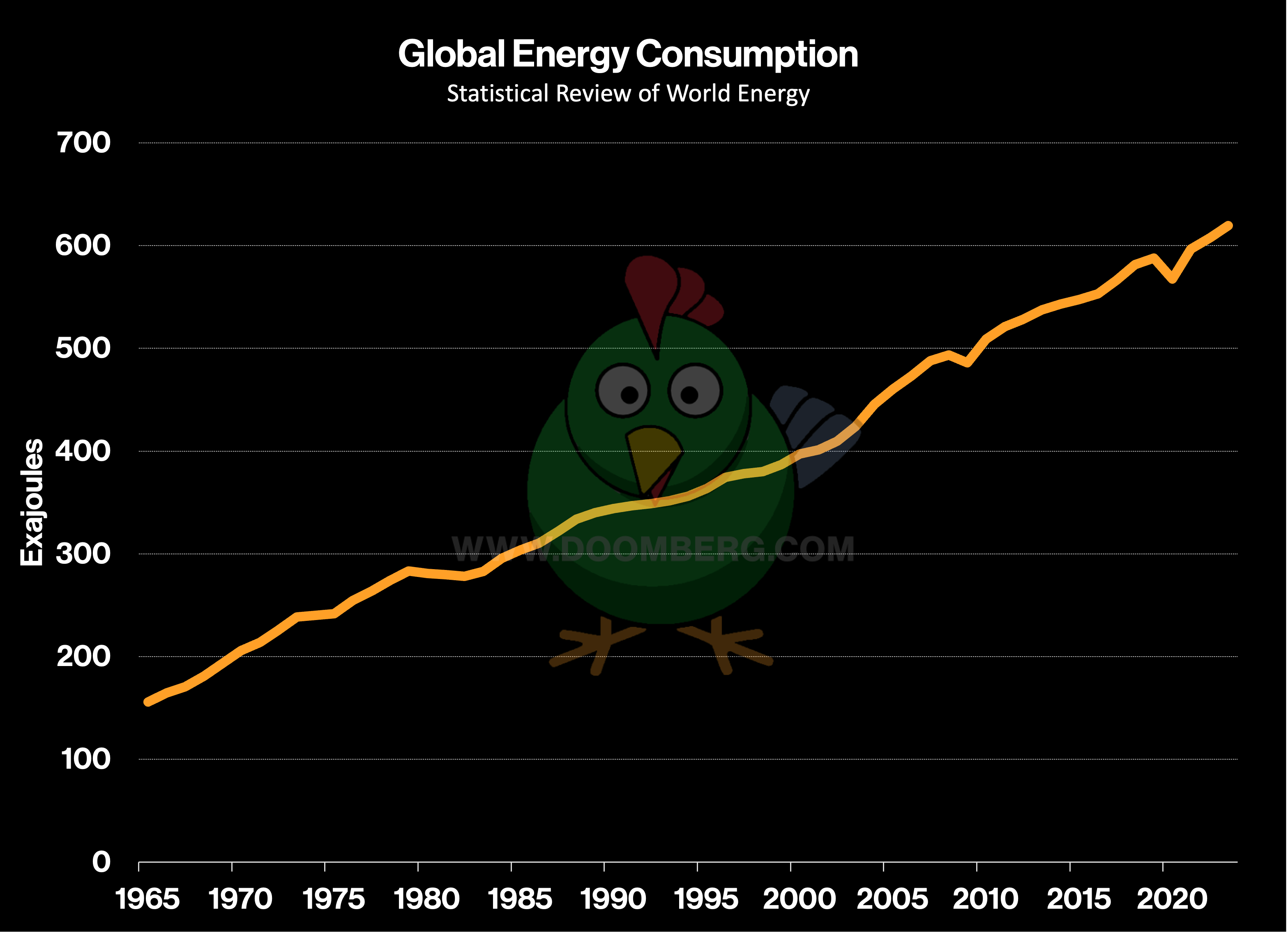

Armed with these four axioms, energy markets no longer appear random or intractable. The grand equilibrium state is roughly knowable in advance. Gluts in one fuel inevitably dampen the price of the others, and the speed of that transmission is but a function of society’s capacity to adapt—a flexibility that is forever improving. The same is true in reverse, of course, and shortages are swiftly met with more than enough supply, causing prices to plunge below where balanced markets would peg them. Since the general economic cycle and the capital investment cycle of the energy sector are perpetually out of phase, an upward-sloping sine wave in global energy consumption emerges, and drawing tangent lines against each curve is perennially a sucker’s bet.

Consider the interplay between oil and natural gas. In January, we published the last of a series of articles explaining why the concept of “peak cheap oil” was a myth, we noted that with proper motivation, all manner of engines would be switched to burn natural gas instead of refined oil products. With the world practically drowning in cheap gas, price spikes in oil would only accelerate the process:

“Given the highly inelastic nature of energy commodities, it would not take much in the way of direct substitution to rein in runaway energy prices should those that adhere to the peak cheap oil hypothesis prove correct. In the long run, every hydrocarbon will be oil, and all will trade for roughly the same price. As a consequence of the most recent energy crisis in Europe, the world will soon enjoy a far more efficient base of natural gas market infrastructure, with LNG export and import terminals connecting far-flung markets in ways that were not possible only years ago. The wide menu of technological and financial solutions available to confront a sudden shortage in oil will similarly ensure that there is more than enough for more than long enough.”

Despite a parade of dire predictions about depleting shale wells, wars in the Middle East, and this-time-we-really-mean-it producer discipline, the world exits 2024 with oil down for the year and clinging to the bottom of its heavily-managed range. As measured in ounces of gold, the stuff has basically never been cheaper. We turn to China for a key reason why:

“Trucking fleets in China are embracing cleaner-burning liquefied natural gas (LNG) for fuel, a trend neighbouring India wants to emulate, accelerating a decline in diesel demand and rattling suppliers to the world's biggest oil importer.

The rise of LNG trucks in China comes on top of world-leading electric vehicle (EV) adoption there and a prolonged economic slowdown, dampening demand in what for decades has been the main driver in oil consumption growth, with crude imports down 2.8% so far this year, weakening global prices.”

In April, we returned to the theme in a piece titled “Generational Arbitrage.” As the name implies, a historic price disparity had broken out between the two fuels in North America. This was driven by global oil prices being held artificially high by the Organization of the Petroleum Exporting Countries (OPEC) and the fact that marginal oil production in the US comes with copious amounts of associated natural gas as a byproduct. Something had to give:

“Fast-forward to 2024 and the North American energy markets are currently experiencing perhaps the single greatest example of hydrocarbon arbitrage the world has ever seen, both in the size of the price differential and the huge volumes involved. We speak, of course, of the vast disparity between the price of domestic natural gas and that of oil. On an equivalent energy content basis, the price of a barrel of oil should be roughly six times that of a million BTUs of natural gas. Accounting for the complexity of handling natural gas, oil has historically oscillated between 10-20 times natural gas. As of the time of this writing, it stands at 45.”

Within two weeks of that article’s publication, the front-month natural gas price at Henry Hub put in its bottom for the year and has more than doubled since. At the same time, oil marked a 2024 top and trended downward to its current level of approximately $70 per barrel. Taken together, these market moves have brought the oil-to-gas ratio back to historically normal levels.

Whether that ratio might eventually reach energy parity—or even plow through it, making natural gas more valuable than oil—was the motivation for “Bridge Burning,” an article published in early October. Although nuclear energy is, by many measures, the ideal technology to power the artificial intelligence (AI) revolution, it does fail in one critically important metric:

“If speed truly is of the essence in the AI race—and few would deny that it is—natural gas is by far the best solution… Will natural gas be the bridging fuel that carries the AI boom along until a full nuclear renaissance can be realized? All the signs are there. At an exponential rate that would surely make Kurzweil smile, the molecule might flip from one that couldn’t be given away to the hottest commodity on the board.”

Building on this concept further in “Irreconcilable Differences,” a piece we published in late November, we speculated that data centers would be built off-grid, out of the purview of federal regulators. Self-contained pods—where natural gas enters one end of a physical structure and data exits the other—would also minimize the inflationary impact of new electricity demand. We then considered who might benefit:

“On the winning side of the ledger sit producers of stranded natural gas in areas like the Permian Basin, where the fuel has sold for negative prices for much of 2024. A wave of distributed power plants constructed next to the cheapest natural gas in the world seems inevitable. In its earnings call two weeks ago, Diamondback Energy put out the word to data center developers that it is open for business....

Gas producers in British Columbia, Canada are also set to benefit handsomely. The province is drowning in the stuff, and co-locating fully-integrated data centers would come with a significant and potentially underappreciated advantage: colder climates make it easier and cheaper to keep the servers cool. Managing heat is one of the most pressing challenges facing data center operators, with some estimates claiming that cooling accounts for up to 40% of the total energy consumed. Any thinking person—lateral or otherwise—can see that this would be a far simpler task to pull off in the Great White North than in the Chihuahuan Desert of West Texas.”

Two weeks later, news broke that validated our dart throw on the board, landing just one province to the west. We’ll take it:

“The province of Alberta, home to the world’s third-largest crude reserves, is making a push to become a hub for artificial intelligence data centres and sees the potential to attract $100 billion in investments.

The government is planning to introduce legislation, make regulatory changes and roll out new services to encourage technology companies to build data centres in the province. The strategy seeks to take advantage of Alberta’s abundance of natural gas for power generation, low taxes and cold climate, which could reduce firms’ cooling costs.”

The holiday season and the turning of the calendar are a time for introspection, reflection, and planning for the year ahead. As 2024 comes to a close and we review the full journey of our thoughts on natural gas as we wrote them over the past year, comparing how our predictions measured up to subsequent events, we hope our paying subscribers feel validated that the investment in our work was worthy of your hard-earned money. If a few of our free subscribers decide to take the leap as a result, all the better!

As for 2025, there is much to cover. The days between now and the US presidential transition on January 20th are fraught with domestic and geopolitical risk—how that event unfolds will have a significant impact on all markets, including energy. We are also keeping a close eye on the pursuit of natural hydrogen, shale development both inside and outside the US, the ongoing accumulation of gold by global central banks, the demographic and resource potential of Africa, and how the imminent election in Canada will affect oil and gas.

When we started Doomberg nearly four years ago, we worried whether there would be enough to write about or if anybody would read our work. More than 340 articles and 275,000 total subscribers later, the verdict is in. Thank you, sincerely, for your readership, and Happy New Year!

“♡ Like” this piece and share it with your most skeptical friend!

Senator Matt Canavan is a brilliant young man and knows the energy portfolio better than anyone in Australia. His strength and conviction which sometimes works against him is that be doesn’t play politics … he says it as it is … which is rare for a politician. Hopefully he’ll be the new energy minister in the next LNP government Downunder … and with a Doomberg subscription on his desk … Australia will be great again!!

Happy new year and keep up the good work!!

In reference to your 13 Nov article entitled "Their Democracy" concerning the Washington state voters approving Initiative 2066, which blocks the state's efforts to impose a statewide ban on that nasty Natural Gas, the expected lawsuits aimed at overturning the election results were filed by King County and the City of Seattle on Dec 11. The suits allege the election result is "unconstitutional" and should be thrown out. And, also as expected, these lawsuits have been joined by the usual "Climate" suspects in expressing their dismay over how wrong the voters are.

Essentially, King County and Seattle are saying the voters got it wrong and so it's their duty to step up and correct the problem. https://www.theolympian.com/news/state/washington/article297006629.html

The case is expected to eventually wind up in the Washington state Supreme Court where the esteemed "Justices" who warm those benches are expected to agree and solemnly announce that Their Democracy is indeed more important than what the voters may happen to think.

This being the same state Supreme Court who in June of 2020, during the mostly peaceful riots, issued a unanimously signed letter expressing their collective anguish over the devaluation and degradation of black lives, and called upon the judicial and legal community to work together to address the lack of racial justice. Eight of the nine who signed this letter are still on the Court. The ninth is retiring, but nobody is worried because a reliable Democrat trial lawyer from Seattle was just elected to take her place. https://www.courts.wa.gov/content/publicUpload/Supreme%20Court%20News/Judiciary%20Legal%20Community%20SIGNED%20060420.pdf

So here in Washington state, we will likely get more of Their Democracy imposed upon us, for our own good, of course. In the meantime, I'll continue to stock up on candles and canned pork-n-beans in anticipation of the looming consequences of our acceleration towards the concrete wall of physics. I'm also checking house/land prices in Idaho...